Why Companies Are Considering Moving Away From PSUs

By Hari Bhatt

April 20, 2026

As discussed in a previous article, ISS recently made a change to its voting policy regarding how it views equity awards that are time-conditioned, especially in relation to the pay mix of time-based versus performance-based awards. Per Voytek Sokolowski in a recently released article on the Harvard Law School Forum website, many corporate issuers would benefit from taking advantage of the new flexibilities provided by proxy advisors like ISS and Glass Lewis.

Proxy Advisory Firm Policy Changes

First, we look at the changes made by proxy advisory firms:

Per ISS:

Time-Based Equity Awards with Long-Term Time Horizon

This policy update reflects the importance of longer-term time horizons for time-based equity awards and provides a more flexible approach in evaluating the equity pay mix in pay-for-performance qualitative reviews.

ISS, when updating their policy, considers market headwinds, changes, and sentiments. If it’s apparent that the market is shifting towards a different set of ‘best practices’, it’s in ISS and other proxy advisory firms’ best interest to proactively adapt to these changes. If they don’t, they risk being seen as reactionary or slow, weakening their position as a trusted source of research.

Per Glass Lewis:

In evaluating long-term incentive grants, prevailing market practice generally indicates that at least half of the grant should consist of performance-based awards, putting a material portion of executive compensation at-risk and that the award should be demonstrably linked to the performance of the company. While LTI program structures that do not meet this criterion are noted, such concerns are unlikely to result in negative recommendations under the Benchmark Policy in the absence of other significant issues with program design or operation.

Changes to program structure which result in significant reductions or elimination of performance based vesting conditions will be assessed on a case-by-case basis. Given the resultant reduction in rigor, if changes are not paired with meaningful revisions to other aspects of the program, such as pay quantum and vesting periods, and/or lack a cogent rationale, they are likely to be viewed negatively by many investors.

Similar to ISS, Glass Lewis has allowed companies leeway to make changes to their equity award programs, and if a company were to reduce the portion of equity awards that are subject to performance metrics, additional disclosure and rationale is expected. Such changes would ‘unlikely’ receive an adverse recommendation on the Say on Pay advisory vote.

Performance-based awards, prior to the recent shift in proxy advisor sentiment, were considered ‘best practice’ if they formed 50% or more of the total equity award package. That is, for every share that is vested based on continued service, one was issued that vested based on one or more performance metrics. Proxy advisors also considered the performance period; that is to say, over what time horizon performance was being measured across to determine payout. Market best practice considered 3 years to be a sufficiently long enough measurement period, and some companies even implemented a 5 year performance period.

Do Performance Metrics Always Reflect True Performance?

As Sokolowski mentions in his article, the last few years have introduced market volatility that is uncharacteristic relative to the years before the pandemic. As a result, there is growing concern that executives may have seen payouts for performance-based equity awards that stray far above or below the ‘target’.

Sokolowski’s argument is especially validated in cases where performance metrics were disproportionately based on relative performance indicators. That is, performance metrics or payout calculations influenced by other companies, indices, or even inflation. For example, the relative Total Shareholder Return (rTSR) metric is widely used as a metric or a modifier. Many companies measure stock price growth as a metric or a performance hurdle, and just as many target a percentile in relation to their proxy peer group. In these cases, and even when measuring revenue, the payout of performance-based awards could be impacted and obscured by the correlation between true company performance and equity payouts.

To mitigate the unintended influences on equity payouts and performance metric outcomes, corporate issuers may consider adapting their equity award programs. Sokolowski has eloquently outlined how companies could gauge investor preferences and slowly adopt changes that incorporate a larger portion of time-based equity versus performance-based equity. In addition, Sokolowski outlines, what he calls, the “1-3-5 PSU” equity award design:

· 1 year to measure performance

· 2 years more years for the award to vest

· 2 years that the equity must be held (colloquially called the ‘holding period’)

This totals to a total of 5 years between when the equity was granted and when the executives can sell their shares.

Taking Advantage of New Flexibility

Sokolowski’s “1-3-5” method touches upon the holding period, a tactic that very few companies have implemented. The holding period is an additional period of time that equity awards must be retained by the executive after they have vested. A performance-based equity award that vested 3 years after grant that is subject to a 1 year holding period would, in effect, be held by the executive for a total of 4 years.

ISS's policies are also relatively qualitative in their assessment of holding periods, and the only qualitative impact comes from a minor scored factor in the Equity Plan Score Card model.

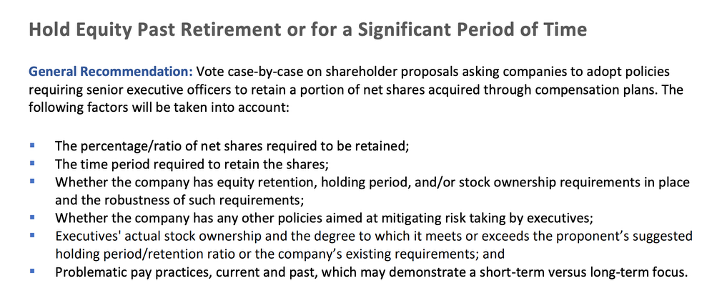

From ISS’s Proxy Voting Guidelines, page 59

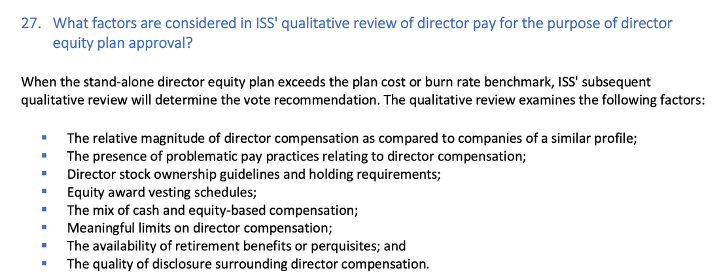

FAQ 27 of the ISS Equity Compensation Plans FAQ

FAQ 36 of the ISS Equity Compensation Plans FAQ

In light of changes to the ISS policy, it stands to reason that companies may take greater advantage of this tactic. Implementing a holding period of 2 years for a performance award that measures over 1 year would be comparable to an award with a 3 year performance period but without the added concern of market volatility affecting years 2 and 3 of performance measurement!

Further, for companies that intend to increase the proportion of time-based awards in relation to performance-based awards, adding a holding period of 1, 2, or 3 years could signal to shareholders and proxy advisors that a company who retains a focus on ensuring executives’ equity compensation remains tied to company performance and stock performance.

However, before these changes can be implemented, or even considered, as Sokolowski mentioned, it’s important to determine if shareholders are open to and supportive of these equity program designs.

How Lioness Consulting Can Help

Whether it’s managing an annual meeting, conducting shareholder outreach, or testing the waters to see if shareholders would respond well to reducing the proportion of performance-based equity awards, Lioness Consulting can help prepare for and help administer your outreach programs. Our seasoned, experienced team has helped many companies just like yours through similar changes in the equity landscape.