What ISS’s EPSC Policy Changes Mean for Your Equity Plan

by Hari Bhatt

March 23, 2026

Have you ever wanted to ask one of those consultants from ISS-Corporate questions about ISS? Figure out what magic number of shares you can increase your equity plan by? Why ISS makes the changes to their Equity Plan Score Card (EPSC) model? I can help. This article can help.

What Changes Did ISS Make to the EPSC Policy?

Per ISS: Enhancements to Equity Plan Scorecard . Adds a new scoring factor under the Plan Features pillar to assess whether plans that include nonemployee directors disclose cash-denominated award limits and introduces a new negative overriding factor for equity plans found to be lacking sufficient positive features under the Plan Features pillar despite an overall passing score.

In other words, the first part of these proposed changes indicates that a new factor will be added to the ISS Equity Plan Score Card (EPSC). The EPSC is (usually) scored out of 100 points, organized into three pillars, with a passing threshold based on the company’s index (S&P 500, R3K, etc). The inclusion of a new factor will lead to a re-weighting of the other factors, and, potentially, the three pillars.

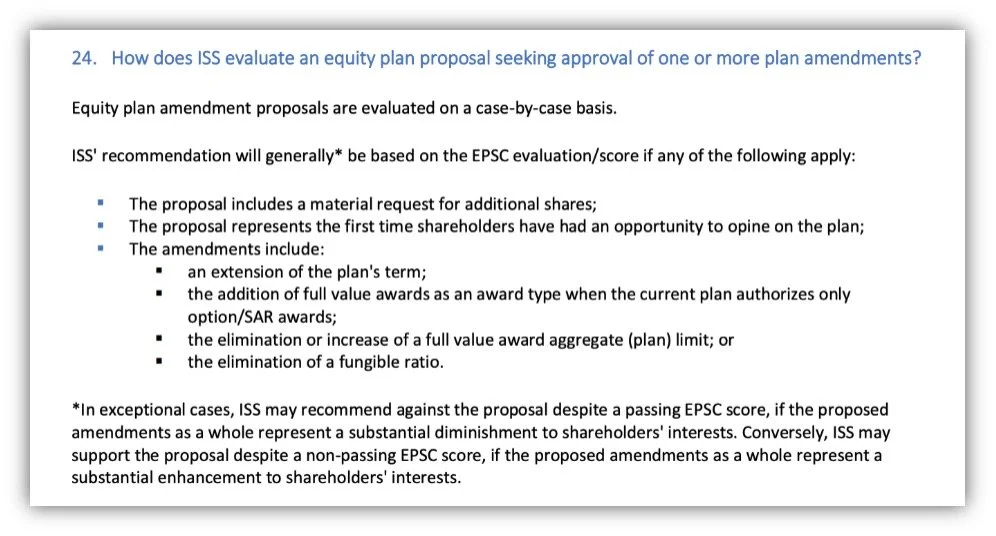

FAQ 24 of the ISS Equity Compensation Plans FAQ

The three ‘pillars’ are essentially three overarching categories that the scored factors are grouped into: Plan Cost, Plan Features, and Grant Practices. The Plan Features pillar takes into account almost all of the policies that ISS assesses on a qualitative level and is the prime category for this new assessment of nonemployee directors' cash-denominated award limits.

I expect that most companies will not receive credit for this factor for one of two reasons: either they do not have or do not disclose the limit for nonemployee directors’ cash awards, or the existing disclosure is not comprehensive or robust enough. It’s likely that over time, more companies will adopt the acceptable policy language as it becomes clear what is considered ‘robust’ (and if the company determines if such a policy is indeed what the shareholders would prefer to have in the equity plan).

The second half of this policy change indicates that a new ‘dealbreaker’ provision will also be included in the Plan Features pillar. The term dealbreaker indicates that ISS will automatically fail the company’s equity plan if not enough points are earned in the Plan Features pillar, regardless of points achieved. I expect the updated ISS Equity Compensation Plans FAQ will outline how many points a company needs to score in the Plan Features pillar to not trigger this dealbreaker.

ISS noted in Appendix B of the Update document that stakeholders indicated that this dealbreaker may unfairly bias towards the Plan Features pillar and undermine the other pillars, which take into account the company’s overhang and burn rate.

Assessment

In my experience, very few companies scored single digit points in the Plan Features pillar, and if they did, their equity plans also included other antiquated policies, such as an evergreen provision (an existing dealbreaker factor in the EPSC), or if the plan permits repricing of options/SARs without shareholder approval (another existing dealbreaker).

I predict only a handful of companies will be directly affected by this policy change, and even fewer will receive an adverse ISS recommendation on their equity plan as long as they make the effort to achieve the threshold score for this dealbreaker provision.

If you need to be sure, contact us to run your EPSC model on ISS-Corporate’s Executive Compensation Analytics (ECA) subscription level. This is not a plug for ISS, but rather for Lioness. Our team of shareholder engagement and corporate governance experts can help review your equity plan, run it through the EPSC model, and provide you with recommendations and outcomes that can potentially increase your share request.

Conclusion

ISS seems to have made the change to their equity plan policy to expand the impact that companies’ equity plans have on director compensation, and to encourage companies to adopt shareholder-friendly compensation policies.

While the second change, regarding a new dealbreaker provision, seems daunting, it’s secretly a blessing in disguise. Say a 100,000 new share request yields an EPSC score of 50 points, and the threshold is 62 points, and the Plan Features pillar is only yielding 5 points. The company would then be forced to adopt or enhance additional policies and rules in the omnibus equity plan, boosting the score. At the same share request of 100,000 shares, the additional plan policies could (theoretically) lead to an EPSC score of 70 points. Then you can maximize the new share request to, for example, 150,000 shares and an EPSC score of 62 points. Not only did the change to ISS’s policy make the equity plan more shareholder friendly, it also led to a larger share request.

It’s worth assessing if your equity plan would gain enough points in ISS’s Plan Features pillar to pass the Equity Plan Score Card model. A second look at your director compensation plans can also help increase your share request. Lioness can help, even if there’s no equity plan on the ballot this year.

We invite you to connect with us to experience the difference of tailored, strategic insights that drive successful outcomes in the dynamic landscape of corporate governance.